The first reaction when thinking of AI and impact might be one of conflict. However, Ascension views this as a huge opportunity, offering a unique and exciting focus - AI is undeniably driving the next systemic shift, much like cloud computing did in its day. This isn't just a technological advancement, but a chance to make a real, positive impact on the world. A great example is Credit Kudos (Ascension portfolio that exited to Apple), which leveraged AI/ML to analyse open banking data, providing more accurate and inclusive credit scores. This innovation was a game-changer, helping lenders better assess creditworthiness and enhancing financial access for underserved individuals.

At Ascension, we’re particularly interested in AI-enabled businesses and datasets that allow lower-income consumers to live better lives, whilst having the potential to become impact ‘dragons’ (fund returners). We’ve seen a number of exciting profit-with-purpose businesses that fit this profile:

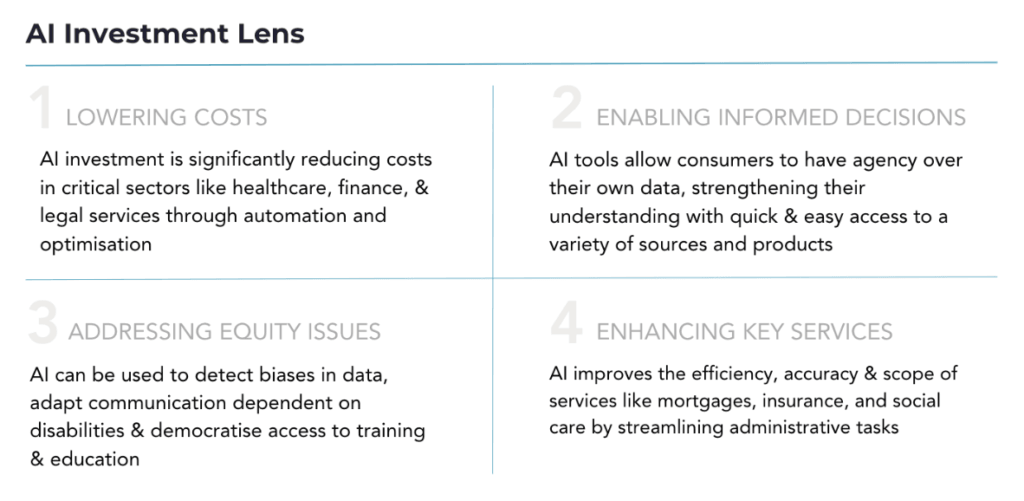

- Lower the cost / increase the quality of delivery for consumers across health, insurance, financial services, legal services and more. A win-win situation where the use of AI provides the end consumer with faster resolution of issues, whilst the service provider spends exponentially less time and resources dealing with them. Ascension-backed CourtCorrect uses AI to streamline and resolve legal disputes efficiently, providing quicker and fairer solutions.

- Enable low-income consumers to make faster & more informed choices. Using AI to provide complete visibility of consumer habits, offering intuitive insights and bespoke recommendations. Ascension recently backed Heatio, a business focused on accelerating the adoption and affordability of decentralised renewable sources of energy; it uses AI to predict energy usage, providing bespoke recommendations to the consumer.

- Increase access to the social mobility ladder. Innovation in technology can be used to help individuals who may not qualify for traditional mortgages to eventually own property through more sophisticated affordability assessments and flexible approaches, leading to savings and enhanced social mobility. We invested in Tembo in 2021, which uses AI-driven technology to analyse hundreds of mortgage lenders and schemes, instantly assessing eligibility and affordability options for buyers. This provides personalised recommendations by scanning over 100 lenders and thousands of mortgage products, helping users maximise their borrowing potential quickly and efficiently.

- Augments the quality of life and the availability & affordability of previously ‘premium’ care services traditionally delivered through the private medical care market. Ada Health (not a portfolio co.) leverages AI to provide personalised health assessments and guidance, offering symptom checking and recommended care steps. In our portfolio, Anathem is automating the administrative burden of mental health clinicians through AI, streamlining the entire workflow so that clinicians can focus on care, not paperwork.

- Solve for huge gaps in health issues such as mental health or women’s health issues. Recent Ascension investment Juniver’s mission is to tackle eating disorders by using AI to reduce relapse rates and maintain healthy eating habits.

- Lower the barriers to accessing education & training. By leveraging AI, high quality and understandable content can be available to a wider audience at the click of a button. Coursera (not a portfolio co.) makes high-quality education from top universities and companies accessible to millions of learners worldwide, democratising access to knowledge and skills development.

What makes a strong AI mission-driven investment opportunity in our eyes?

- Application with defensibility: look beyond the standalone consumer layer or ‘enablers’, seeking proprietary data insights combined with a founding team with a deep understanding of the stakeholders using and engaging with said data. Unfortunately, the low barriers to integrating AI co-pilots make them easily replicable, but the founding team's expertise is crucial for swiftly and effectively creating valuable commercial outputs.

- Commercial & technical sector knowledge: this could relate to years of data being tracked in a certain sector vertical & using Generative AI to leverage that dataset. We are currently assessing a company using an existing proprietary dataset to address issues related to Menopause and Endometriosis as their beachhead use case.

- The pain is deep and acknowledged: search for places where AI is coming at a point where the problem is felt very deeply and the consumer/customer is ‘ready’ to adopt it as a result.

- Infrastructure layer or line of sight to the impact on the end consumer: when assessing a new investment opportunity, we need to see a line of sight to how scaling the innovation will reach a mass market audience, including lower-income consumers. As an impact investor, a lot of the business models we back are B2B2C with a clear path to reaching these people, but we also often look at B2B innovations changing the system around the consumer. A good example of this is Credit Kudos which sold B2B into banks and used Open Banking to make access to credit more affordable. Although the business model didn’t link to consumers directly, we could measure the direct impact of the innovation on the consumers’ social fabric. This is similar to how we approach investing in AI. We assess the ‘infrastructure layers’ of AI technology that are applied in specific sectors and have technical founders that are deeply passionate about reaching that group.

To summarise, although application layers are less capital intensive, we look for a defensible moat such as: 1) sector expertise with specific regulation and hard-to-replicate language; 2) founders with unique insight and deeply embedded in the routes to market & user journeys, leading to speed of execution; 3) proprietary enriched data either built through prior years or added by the consumer.

Considering risks in AI for low-income consumers

While there is exciting potential for AI to positively impact the lives of consumers in a multitude of ways, we recognise that AI won’t always create positive outcomes - with automation threatening certain jobs and the decline in human intervention potentially affecting more vulnerable customers. However, we believe that the potential positive impact of AI far outweighs the negative. Those ‘market failures’ and risks also present opportunities for innovation, such as enabling banks to rethink financial services delivery by concentrating human support on vulnerable customers.

This is why being very specific with our fund’s theory of change of reducing social inequalities for lower-income communities by 1) helping them earn more, 2) reducing their cost of living or 3) improving their health, allows us to keep our target audience in mind at all times.